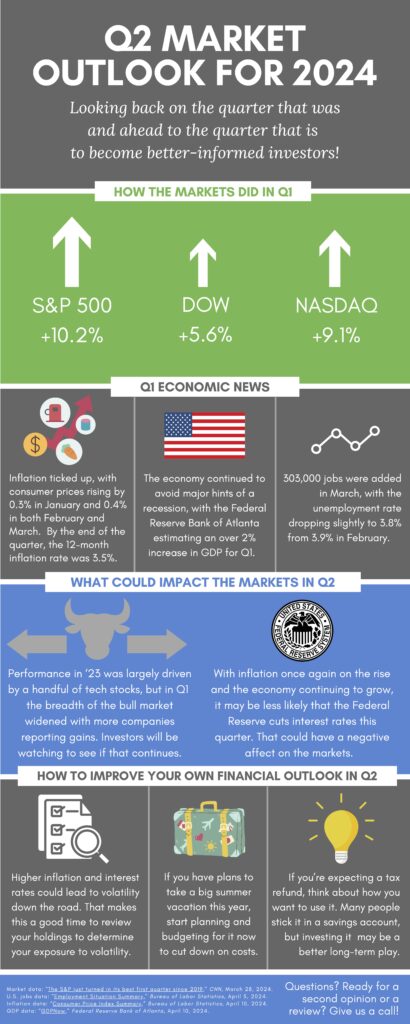

The Pale Blue Dot

On February 14, 1990, the Earth was being watched.

The object watching Earth was small; small enough to fit inside a four meter-large cube. And it was distant, being over 3,000,000,000 miles away. It is even farther away now—in fact, it recently became the first man-made object in history to venture into interstellar space.

It was the Voyager 1 spacecraft.

Voyager 1 is a probe built by NASA, launched in 1977 to study the outer Solar System. Its primary mission was to study the planets Jupiter and Saturn and their various moons. Having accomplished this, the probe is now winding down its secondary mission, which is to study the distant regions beyond the planets before it loses power and becomes destined to drift through the Universe as a mute, lonely messenger until the end of time.

But this post isn’t about Voyager. It’s about Earth.

On that date in 1990, Voyager 1 had completed its primary mission. Carl Sagan, the famous astronomer, and author, asked NASA to turn the probe’s camera around to take one last photograph of Earth and the other planets. Between February 1 and June 6, Voyager took sixty still images. Each image contained about 640,000 individual pixels, and as the probe was so far away, it took about 5½ hours for each pixel to reach Earth.

The most famous of these photographs was of our home planet—now just a pale blue dot amidst the infinite blackness of space.

If you’ve ever seen this photo, you know what a stirring, thought-provoking image it is. Imagine our great, grand planet … filled with life, oceans, mountains, deserts, forests, and cities, reduced to nothing more than a speck. It serves to illustrate just how small we really are compared to the unceasing vastness of the Universe. But it also serves another, more powerful purpose.

April 22 is Earth Day, a celebration of our planet, of nature, and of the importance of protecting the environment. Hundreds of thousands of people will observe the event in their own way, but many more will probably fail to remember that Earth Day exists at all. After all, there are already so many holidays demanding our time, our attention, and our money. Most of us probably don’t even get Earth Day off from work.

And yet, we wonder if we wouldn’t attach more importance to Earth Day if we all took a few minutes, once a year, to simply look at that pale blue dot. Because there’s something else the picture illustrates, something we should all remember.

Take a minute, to pull up the picture on your computer. Search for “pale blue dot” on Google® or go to this address at http://en.wikipedia.org/wiki/Pale_Blue_Dot to see it directly. After you look at the single pixel that is our planet, gaze around the edges of the image. What do you see?

Nothing.

Of course, we know that the Milky Way galaxy isn’t empty. It’s bursting with stars, cosmic rays, solar wind, clouds of dust, asteroids, comets, and even other planets. But it contains no other life, not that we’ve found. The closest planet potentially capable of supporting life is so far distant, it would take millions—millions!—of years to get there. That’s longer than our species has even been alive.

Until further notice, we are alone.

Our pale blue dot is just one of billions in the night sky, but it is unique. We are on an island amidst a dark, silent ocean. An oasis inside the barrenness of space. A single, precious garden surrounded totally by desert.

What the pale blue dot photo really shows is that our planet is significant. It’s all we have. It shelters us, sustains us, provides for us, and entertains us. If there is another world richer and more beautiful than ours, we’ve yet to find it.

In short, we’ve been given the greatest gift of all.

This is why Earth Day is important: because it’s our chance to reflect on what we can do to truly deserve that gift. It is our chance to reflect on how we can protect it, because it certainly needs protecting.

This April 22, we invite you to celebrate Earth Day. Even if you do nothing else but feel the warmth of the Sun on your face, smell the flowers in bloom all around you, and ponder the depths of the night sky, it will be enough.

And as you celebrate Earth Day, ponder the words Carl Sagan left us about our precious, pale blue dot.

The Earth is the only world known, so far, to harbor life. There is nowhere else, at least in the near future, to which our species could migrate. Visit, yes. Settle, not yet. Like it or not, for the moment, the Earth is where we make our stand. It has been said that astronomy is a humbling and character-building experience. There is perhaps no better demonstration of the folly of human conceits than this distant image of our tiny world. To me, it underscores our responsibility to deal more kindly with one another and to preserve and cherish the pale blue dot, the only home we’ve ever known.

Carl Sagan, Pale Blue Dot: A Vision of the Human Future in Space (Ballantine Books, 1994)

On behalf of all of us here at Minich MacGregor Wealth Management, Happy Earth Day!